by Michael P. Broxterman, COO &

Wendy Abdo, Staff Writer – Pinnacle Health Group

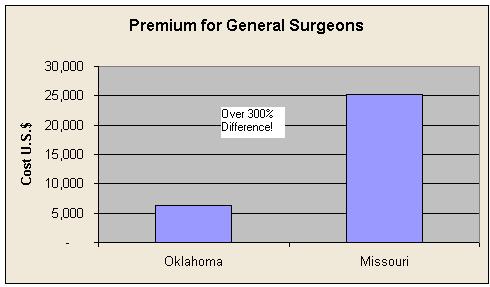

People are on edge about the sharp rise in malpractice insurance premiums. Many physicians have limited their clinical services or have even relocated to more equitable practice environments. Because of this, some hospitals in crisis states are concerned about overcoming physician recruitment obstacles and remaining competitive with other hospitals in non-crisis states. To Illustrate the gap between crisis and non-crisis state premiums, we have collected the following data to serve as a snapshot cost estimate of first-year claims made premiums for a General Surgeon.

According to a leading malpractice insurance company, estimated coverage for a General Surgeon in Oklahoma based on a $1 million/$3 million limit is $6,256. In contrast, the same General Surgeon operating in Missouri with identical coverage would have to pay $25,195 for a first-year claims made premium. If this General Surgeon decided to move from Oklahoma to Missouri, he/she would be paying over 300 percent more for malpractice insurance. Another point to keep in mind is that premiums tend to double or triple over a standard five-year maturity period. Physicians are all too aware of these costs. If a doctor is looking at several different employment opportunities, the cost of malpractice premiums may be instrumental in making his/her final decision. However, doctors who move across state borders are not the only ones touched by the volatile malpractice market.

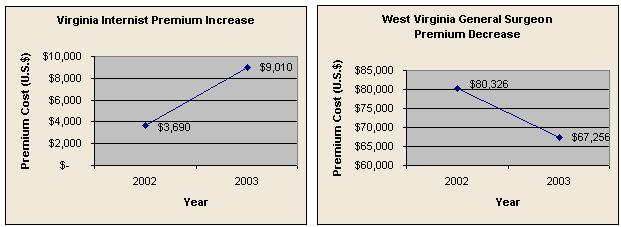

Physicians, who decide to stay where they are, have also been affected. In particular, Medical Liability Monitor has reported that Internists in Virginia have seen a 144.2 percent increase in mature claims made malpractice rates from 2002 to 2003 ($3,690 to $9,010) as shown above. But were there any rate decreases reported? Yes. In fact, West Virginia’s General Surgeons went from paying $80,326 in 2002 to $67,256 in 2003; a 16 percent decrease. According to the study, Florida rates were the highest in the country with mature claims made rates for General Surgeons topping out at a whopping $226,542.

A Gynecologist in Nebraska making $250,000 a year paying $16,194 for malpractice insurance who moves to Illinois where malpractice premiums are $147,023, will lose a mind boggling $130,829 a year! If compensation does not adequately cover this increase he/she will not contemplate the move. Therefore, it is important for hospitals to consider all alternative compensation methods in their recruitment strategy.

So what can hospitals that are located in crisis states do to “sweeten the pot” for prospective candidates? They can do the following:

1) Agree to pay the physician’s malpractice insurance for a designated length of time,

2) provide adequate “tail” coverage for the physician,

3) agree to compensate by increasing base salary, or

4) offer a signing bonus that will cover the costs of the malpractice insurance.

Another significant factor that affects compensation is the hospital’s payor mix. If the payor mix compares favorably, this difference will help reduce the worries a physician may initially have in moving to a high premium area.

Writers of professional medical liability insurance tend to be pessimistic about current and near future malpractice rates. According to Medical Liability Monitor, 83 percent believe that more rate increases will happen in 2004. However, they do not think it will be as high as it was in recent years.

Is there light at the end of the tunnel? Yes. Regardless of these issues, national and state-level tort reform efforts should eventually stabilize the current situation. Likened to our own economy, malpractice premiums go through cycles. In almost every decade since the 1960s, a problematical malpractice situation has taken place at some point. All states now have tort reform on their legislative dockets. Results are forthcoming. In addition, public attitudes seem to favor tort reform. A recent Gallup pole indicated that 72 percent of Americans believe in limiting the dollar amount a patient can be awarded for “pain and suffering” damages.

Physicians should not be quick to rule out a job opportunity just because it is located in a crisis state. Even in average years, malpractice premiums will vary, sometimes considerably, from year to year, state to state, and county to county. Hospitals and medical facilities must be knowledgeable about each candidate’s malpractice insurance rate. By keeping this in mind while drafting the contract, hospitals can ensure their offer will be seriously considered. As with every position, there are good points and bad points. What you must focus on is the overall balance. If physicians will be getting 80 percent of what they initially wanted then their decision to accept the job opportunity will most likely be a good one.

References

Medical Liability Monitor. (October 2003). Rate Report Presents State-by-State Snapshot of Changing Market. Volume 28, No. 10.

The New England Journal of Medicine. Coping With Malpractice Coverage Issues. Retrieved November 9, 2003, from

http://www.nejmjobs.org/resource_center/article_24.asp.